Summary

There are three types of home loan websites available to you today:

- Lead generation websites collect information to sell to mortgage lenders, banks, and brokers in exchange for a fee.

- Mortgage lender websites are designed to get you to apply for a mortgage with them.

- Traditional banks offer a variety of financial products, including mortgages, but they may not cover all the home equity products. They also tend to have higher rates and fees.

Each has their own pros / cons and in this post we synthesize the differences, and compare each to House Numbers.

Homeowners have access to a wide range of online resources when learning about their home equity, especially when they are trying to access their equity. It gets very confusing because there are so many different types of services competing for their business, each with a different value proposition and offerings. To make matters worse, many have horrible rates, while others present teaser rates that only apply for the first few months of the loan.

To better understand the home equity loan landscape, we decided to write a post about how to distinguish the difference between each of these sites vs House Numbers, and how you should proceed when searching for a loan. The three types of companies homeowners visit online for information about accessing their home equity are:

- Lead generation websites

- Mortgage lenders

- Traditional banks

Below, I’ll explain the difference between the three types and how they compare to House Numbers.

Find the best way to unlock home equity

Lead generation websites

Lead generation websites have a wide variety of generic information about homeownership and endless requests for your personal information. Why? Because that’s how they make money. Once you enter your information on one of their lead generation forms, it gets sent to various mortgage lenders, banks, and brokers who will contact you to earn your business (whereas with House Numbers, we never share your info).

The most well-known lead generation websites are:

- Bankrate

- LendingTree

- Nerdwallet

- CreditKarma

We recommend clients and homeowners avoid these sites at all costs. As we discuss below, you will be hit with more phone calls, texts, and emails from their partner lenders than you can handle.

Lead generation website structure

These four websites are generally structured the same. There is a mix of content to engage the user, but the rate table is the main attraction. Thousands of pages with “rate tables” listing individual mortgage companies and the unverified mortgage rates they offer. These tables are spreadsheets listed on a webpage, like a stylized Excel spreadsheet, to keep you, the reader, entertained.

The individual mortgage companies provide a rate and APR based on the lead generation website preset criteria (location, purpose, loan amount, loan-to-value ratio, and credit rating). Don’t be fooled! None of these rate quotes are personalized to you! This frustrates us at House Numbers because we always provide an accurate, real-time rate quote personalized to you after you enter your information. Lead gen websites don’t have the same technology access that we have so they are not able to give you the same level of personalization.

Furthermore, you’ll also notice on lead generation websites an area that lists “total fees”; however, if you dig a little deeper, you’ll find out that the amount listed does not include your total fees. Looking at Nerdwallet, you will see “total fees” listed; however, if you click on the “?” with a circle around it, you’ll see a disclaimer that says, “Other third-party fees may apply.”

Like Nerdwallet, Bankrate has a fee listing within their rate tables. The fee section for each mortgage is labeled “Upfront cost,” yet third-party fees are noticeably missing. What are third-party fees? These are fees charged to you by a company or person that is not the lender. For example, an appraisal fee and a title search are considered third-party fees.

I could go on forever why we advocate against using lead gen companies so here are just a few remaining points of why House Numbers is better:

| House Numbers | Lead Gen Websites |

|---|---|

| Easily apply online, from the comfort of your home, at your convenience. | Cannot apply online |

| We never sell your contact information. | Entire business model is from selling your information to the highest bidder |

| Regulated by federal and state agencies as licensed mortgage broker. | Not regulated, not a broker, very little government oversight. |

| Offers multiple home equity products. | Very few sites offer home equity products and rates. |

| Receive personalized, real-time rate quote for your specific needs. | Only offers generic range of rate quote. |

How do lead generation websites make money?

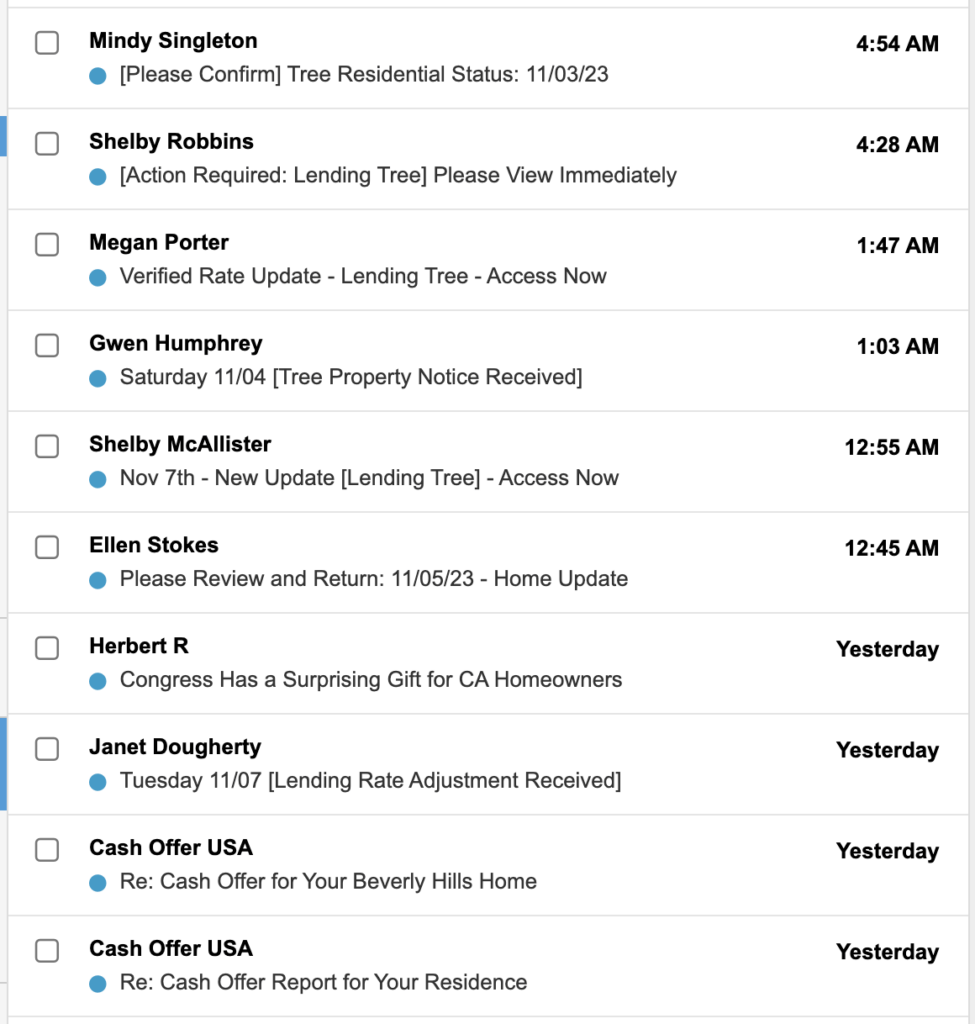

Lead generation websites make money in a few different ways, with the most popular being lead sales (in other words, they will sell your information to the highest bidder!). Remember those fancy rate tables we mentioned above? Well, those tables are designed to get you to click a button and enter your personal information so that the lead generation website can earn a fee by selling this information to a mortgage lender, bank, or broker.

When you click to get a quote and enter your contact info, you typically will get four to eight mortgage companies contacting you about their services almost immediately. This is most common with LendingTree.

| |  |

Once you complete the process of entering your information, it is sent to the lender for them to contact you about their services. Before a homeowner enters their information, it’s important to know the downsides associated with lead generation websites:

- You will be bombarded with calls, texts (SMS), and emails immediately

- Your information will be sold multiple times over the year

- The mortgage rates are unverified and listed fees are estimated

- The “offer” is not legitimate — it’s an estimate (Read the fine print!)

- Not all home equity products are covered

- No direct online application (you must speak to agents by phone and email)

To make matters worse, the inbound emails, calls, and texts seem to multiply as time goes on! The lead generation website will resell your information as an “aged lead” to additional mortgage companies. These “aged leads” cost the mortgage company less than if they were to purchase your information as an initial real-time inquiry.

Find the best way to unlock your home equity

House Numbers helps you access your home equity to pay off debt, fund home improvement, or general expenses.

Mortgage lender websites

Mortgage lender websites are different from lead generation websites. Mortgage lender websites are mortgage companies that provide mortgage loans to homeowners, and how they make money compared to lead generation websites is different. They make money by getting you to do a loan with them (whereas lead gen websites sell your information to make money). Nonetheless, even though these sites may be a step above the lead gen websites, they still fall short of House Numbers because they only offer you rates from their own company — House Numbers searches the market in your area to ensure you are getting the best deal that fits your needs! In other words, they are a single lender and House Numbers is a broker so we can work with multiple lenders. Some of the most popular online mortgage lenders include:

- Rocket Mortgage

- Better

- Guaranteed Rate

- LoanDepot

Mortgage lender website structure

The design of these websites is simple; they want the homeowner to either request a rate quote or apply for a mortgage. To do this, their website has three main types of pages:

- Informational pages

- Article pages

- Landing pages

Information pages on mortgage lender websites are web pages that are stylized and provide bits of information to the homeowner. Typically, you will see loan program pages like this, such as FHA or VA home loan pages.

The mortgage lender will design the page so that the homeowner gets the gist of the program and is inspired to request a quote or complete an online application. It’s important to know that not all FHA and VA home loan pages are like this; some websites choose to write an article instead.

The article pages are self-explanatory. The page’s topic is covered in article format, and the “Call To Action” (CTA) sections are within the article. The goal of their CTA is to nudge the reader to request a quote or apply for a home loan. Article pages are typically about topics that are relevant to the mortgage industry, such as “How to increase your credit score to get a better rate.”

Landing pages are pages specifically designed for marketing and advertising campaigns. Mortgage lender websites design these pages to sell a produce or service, grabbing a homeowner’s attention quickly so that they will convert immediately. These pages are designed with the least possible information, and the focus is on the style and visual impact of the page.

Working with an online direct mortgage lender has its benefits; however, there are some downsides.

- They don’t cover all the home equity products

- You only receive one offer from one lender (House Numbers can search for multiple offers)

- Limited ability to go outside of the box (i.e. any complications or unordinary circumstances with your loan will lead to rejection)

- Some loan officers are new to the business

- They usually won’t provide a quote without a credit check

- High pressure so you’ll commit quickly to the loan

- Require a credit card upfront before moving forward

- Assembly line process to closing your loan/lots of different people calling you

Why do they require a credit check to give you a quote? It’s a sales tactic that gets you to commit to moving forward with their loan option. Many homeowners want to avoid more than one credit check, and these lenders know that, so they ask for that upfront before the quote. Another sales tactic is to demand that the homeowner provide a credit card number before moving forward. This is another way to get you to commit to their loan and not shop around.

When homeowners investigate their options for leveraging their home equity, they should be provided with a wide variety of home equity products, and these online mortgage lenders are not equipped to do that. Homeowners need more than one offer from an inexperienced loan officer and should not be pressured into a loan option that doesn’t meet their needs.

Traditional bank websites

Everyone knows of Wells Fargo, Bank of America, and other banks that provide mortgage products to homeowners. Here are the well-known traditional banks with a significant presence online.

- Wells Fargo

- Bank of America

- Chase

- Citibank

Traditional banks offer everything from credit cards to personal loans, mortgages, and more. Homeowners who want to leverage their home equity into a future investment may think a traditional bank would be the right choice; however, there are some drawbacks:

- They don’t cover all the home equity products

- You only receive one offer from one lender

- Generally slow to process your application

- Lack of efficiency when processing your loan application

- Rates and fees might be higher

- Rigid underwriting guidelines

Did you know there are some equity products, like Home Equity Investment, that traditional banks don’t offer? And when you work with your bank, you will miss out on competing offers on the products they have. Traditional banks are not known for fast processing, which is why so many homeowners look at other options for their home equity needs. Traditional banks typically charge higher rates and fees, and their underwriting guidelines do not allow for an outside-the-box, common-sense approach to underwriting.

Banks know the average homeowner’s first instinct is to work with their bank, so they have little incentive to be competitive with product offerings, rates, processing times, and underwriting standards.

House Numbers is the best way to shop for a 2nd mortgage

Utilizing your home equity to increase wealth is a game changer for most homeowners. Knowing which online resources will help you achieve that goal is a key part of the process. Lead generation, mortgage lenders, and traditional bank websites come up short compared to House Numbers. Give us a try today to understand why we are a level above the rest!