Summary

- Home Equity Agreement or Home Equity Investment is a way for homeowners to tap into their home equity without increasing their monthly payments.

- The homeowner sells a share of their home to investors in exchange for access to the future appreciation of their home.

- Since it’s in investment, and not a loan, the homeowner doesn’t need to pay anything back until they sell the property, in which case, the investors share in the home’s appreciation.

- We partner with Unlock and recommend them to all our clients. They are an affiliate of ours and many of our clients have reported success with them

Equity sharing agreements — also known as home equity investments (HEI) — are a relatively new and often misunderstood way to get cash from your home equity. Below I will explain what they are, how they work, and why this is a product of last resort.

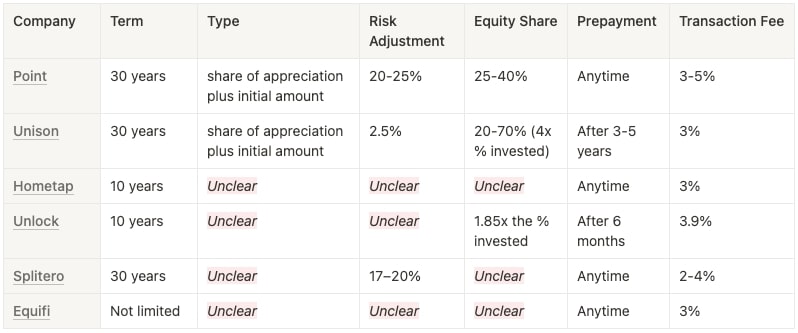

As always, the details matter, and there can be a big difference between lenders! So, let’s take a closer look.

| Company | Term | Type | Risk Adjustment | Equity Share | Prepayment | Transaction Fee |

| Unlock | 10 years | Unclear | Unclear | 1.85x % invested | After 6 months | 3.9% |

| Point | 30 years | Share of appreciation plus the initial amount | 20 – 25 % | 25 – 40 % | Anytime | 3 – 5 % |

| Unison | 30 years | Share of appreciation plus the initial amount | 2.5 % | 20 – 70 % (4x % invested) | After 3 – 5 years | 3% |

| Hometap | 10 years | Unclear | Unclear | Unclear | Anytime | 3% |

| Splitero | 30 years | Unclear | 17 – 20 % | Unclear | Anytime | 2 – 4 % |

| Equifi | Not limited | Unclear | Unclear | Unclear | Anytime | 3% |

How do Home Equity Investments work?

In principle, an HEI helps you “sell” a share of your home equity to an investor for cash that you receive up-front. The investor typically makes money from “shared appreciation”: your home goes up in value over time and, when you sell or refinance your home or the term of the HEI expires after 10-30 years, the investor receives a percentage of that increased value.

Sound too good to be true? These are investors, after all, so there are protections built in to help ensure that they don’t lose money. In many cases, this means they discount the value of your home and get paid back most or all of the cash you receive up-front even if your home does not go up in value.

When do you pay back the HEI?

There are variations between providers, but typically the HEI has a term of 10 to 30 years. At the end of the term, you normally have to buy out the investor’s share of your home via a cash-out refinance, home equity loan, or by selling your home. Most providers do not have a prepayment penalty, so you’re free to buy them out before the end of the term if you’d like.

What are the main benefits?

- Continue to own and live in your home

- Receive cash up-front

- No monthly payments

- No minimum income requirements

- If your home goes down in value, you owe less

What are the main drawbacks?

- If your home increases in value a lot, the HEI becomes more expensive. Because you are selling a share of the upside in your home, the more your home is worth, the more you end up paying the HEI investor. This should also make you think twice about an HEI if you’re planning a big remodel to your home that will increase its value a lot.

- The investor will often discount the real value of your property. The investor normally applies a “Risk Adjustment” to protect their initial investment, in case the appraisal is wrong or the housing market changes quickly. So, if your home is worth $500,000, you may only get the benefit of as little as $375,000.

- Transaction fees. In addition to an appraisal and escrow fee, a 3-5% transaction fee will normally be deducted from your funds. Depending on the amount you are receiving, this could be quite high compared to a cash-out refinance, HELOC, home equity loan, or reverse mortgage.

- HEIs are only available in select areas. HEI investors pick markets and states they think are good bets and, because this is a new product, their overall geographic coverage is low.

- Your current mortgage may not allow it. Although you remain the owner of your home, the HEI provider will confirm your mortgage doesn’t prohibit this type of arrangement.

- It often limits your ability to refinance or take out additional home equity. This may be because the HEI must be paid back when you refinance, or because the contract limits the overall amount of debt you can have on your home.

- The terms are often complicated. Unlike cash-out refinancing, reverse mortgages, HELOCs, and HE loans, HEIs are not standardized. Every company does things a bit differently…even though one term of the offer may look better, they likely make it up somewhere else. It’s important to run the numbers and compare proposals to find the best option for you.

Who are the main lenders & investors, and what do they offer?

Below is a table of the main providers of HEIs. As you can see, the key terms vary quite a bit and the providers are not very transparent about how these products work.

So, it’s important to get multiple offers and consult with someone knowledgeable to run the numbers for YOUR situation. House Numbers can help!